In the journey toward homeownership, understanding how mortgage interest rates are determined is essential. Factors such as credit score, loan type, and economic conditions play a crucial role in determining the interest rate you will be offered. Bad Credit Loan specializes in providing tailored mortgages for individuals with diverse credit backgrounds. With a user-friendly online platform, customizable options, and transparent practices, Bad Credit Loan empowers individuals to achieve their homeownership goals, regardless of their credit history. From purchasing a dream home to refinancing for better terms, Bad Credit Loan stands ready to support borrowers every step of the way.

.")

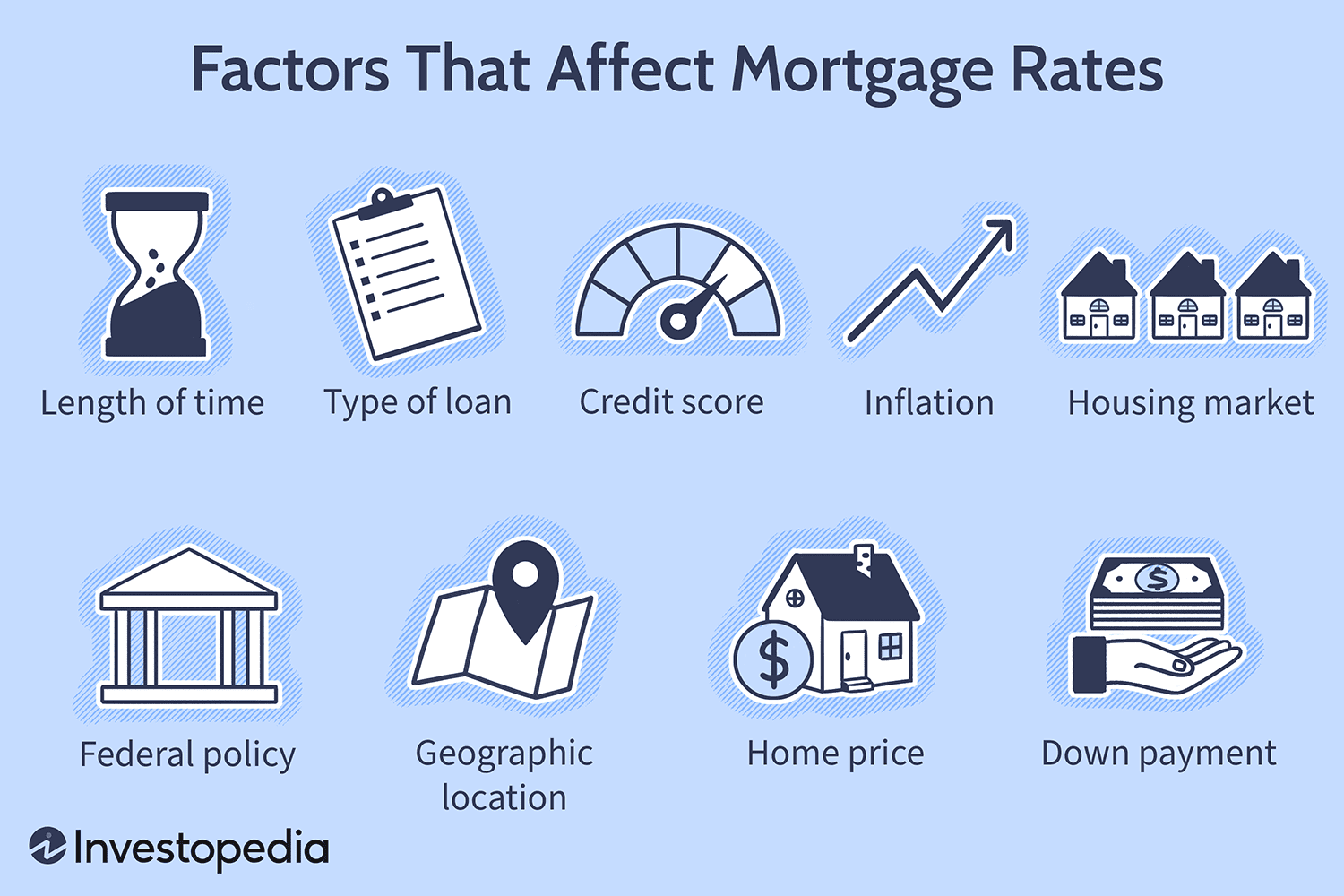

Credit Score

Your credit score plays a significant role in determining the interest rate you will be offered on your mortgage. Lenders use your credit score to assess your creditworthiness and determine the level of risk they will be taking by granting you a loan. A higher credit score indicates a lower level of risk, which translates to a lower interest rate. On the other hand, a lower credit score suggests a higher level of risk, leading to a higher interest rate.

To determine your credit score, credit reporting agencies analyze various factors including your payment history, credit utilization, length of credit history, types of credit, and new credit inquiries. It is important to regularly review your credit report and ensure that it accurately reflects your financial behavior. By maintaining a good credit score through timely payments and responsible credit management, you can increase your chances of securing a mortgage with a favorable interest rate.

Loan Type

The type of mortgage loan you choose will also impact the interest rate you are offered. There are various types of mortgage loans available, each with its own characteristics and interest rate considerations. It is essential to understand the differences between these loan types to make an informed decision.

Fixed-rate mortgages have a stable interest rate that remains the same throughout the life of the loan. This provides predictability and allows you to budget your monthly payments with certainty. Adjustable-rate mortgages (ARMs), on the other hand, have an interest rate that can change periodically. Initially, ARMs may offer lower interest rates, but they can increase over time, potentially leading to higher monthly payments.

When deciding between fixed-rate and adjustable-rate mortgages, consider factors such as your financial stability, long-term plans, and risk tolerance. If you prefer the predictability of steady payments, a fixed-rate mortgage may be more suitable. However, if you anticipate selling the property or refinancing the mortgage before the adjustable rate period begins, an ARM could provide short-term savings.

")

This image is property of www.investopedia.com.

Economic Factors

Economic factors play a significant role in determining mortgage interest rates. Two key economic factors that influence interest rates are inflation and the Federal Reserve’s monetary policy.

Inflation is the increase in the general price level of goods and services over time. When inflation is high, lenders may raise interest rates to compensate for the decreasing purchasing power of money. On the other hand, during periods of low inflation, interest rates may be lower to stimulate borrowing and spending.

The Federal Reserve, as the central bank of the United States, plays a crucial role in shaping the economy and interest rates. By adjusting the federal funds rate, the rate at which banks lend money to each other, the Federal Reserve can influence the cost of borrowing for financial institutions. Changes in the federal funds rate can have a cascading effect on mortgage interest rates, causing them to rise or fall.

Market conditions also affect mortgage interest rates. Supply and demand dynamics, investor sentiment, and global economic trends can lead to fluctuations in interest rates. During periods of economic uncertainty, lenders may increase interest rates to mitigate risk, while favorable market conditions can result in lower interest rates.

Down Payment

The down payment amount you contribute towards the purchase of a home can impact the interest rate you are offered on your mortgage. A larger down payment generally leads to a lower interest rate. When you make a larger down payment, you demonstrate financial stability and reduce the lender’s risk. As a result, lenders may reward you with a lower interest rate.

The loan-to-value (LTV) ratio, which compares the loan amount to the appraised value of the property, also affects interest rates. A lower LTV ratio indicates a lower level of risk for the lender, potentially resulting in a lower interest rate. By making a larger down payment, you can reduce the loan amount and improve your LTV ratio, increasing your chances of securing a more favorable interest rate.

")

This image is property of fastercapital.com.

Loan Term

The term of your mortgage loan, or the length of time over which it will be repaid, can impact the interest rate you are offered. Generally, shorter-term loans, such as 15-year mortgages, tend to have lower interest rates compared to longer-term loans, such as 30-year mortgages.

Shorter-term loans typically come with higher monthly payments but result in lower total interest paid over the life of the loan. On the other hand, longer-term loans offer lower monthly payments but result in higher total interest paid over time.

When choosing the loan term, consider your financial situation, long-term goals, and ability to make higher monthly payments. If you can afford higher monthly payments and want to save on interest costs, a shorter-term loan may be more suitable. However, if you prefer lower monthly payments to accommodate other financial obligations, a longer-term loan may be a better option.

Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is an important factor that lenders consider when determining your mortgage interest rate. The DTI ratio compares your monthly debt payments to your gross monthly income. Lenders use this ratio as an indicator of your ability to manage mortgage payments in addition to other financial obligations.

A lower DTI ratio indicates that you have more disposable income available to meet your mortgage payments. Lenders typically view a lower DTI ratio as less risky, potentially resulting in a lower interest rate. On the other hand, a higher DTI ratio suggests a higher level of risk, leading to a higher interest rate.

To calculate your DTI ratio, add up all your monthly debt payments, including credit cards, student loans, and car loans. Then, divide that total by your gross monthly income. If your DTI ratio is high, you can improve it by paying down debts, increasing your income, or reducing your monthly expenses. Lowering your DTI ratio can not only increase your chances of securing a mortgage but also improve the interest rate offered.

")

This image is property of www.investopedia.com.

Property Type

The type of property you are purchasing can impact the interest rate you are offered on your mortgage. Lenders assess the risk associated with different property types and adjust interest rates accordingly.

Single-family homes generally carry lower interest rates compared to condos or multi-unit properties. Lenders consider single-family homes to be less risky due to their potential for higher appreciation and ease of reselling. Condos or multi-unit properties often come with higher interest rates as they can be subject to additional risks such as association rules, maintenance costs, and rental income uncertainties.

Lenders assess the risk associated with the property type based on their experience and market trends. It’s important to consider the potential impact of property type on your interest rate when deciding between different housing options.

Location

The location of the property you are purchasing can affect the interest rate on your mortgage. Regional housing markets and their associated factors can influence interest rates.

In areas with strong housing markets and high demand, lenders may offer lower interest rates to attract borrowers. Conversely, in areas with less demand or uncertain market conditions, lenders may increase interest rates to mitigate risk.

Assessing property values and risk in different areas is essential when considering location-based interest rate fluctuations. Consult with a real estate professional or conduct research to understand the local housing market dynamics and their potential impact on mortgage interest rates.

")

This image is property of fastercapital.com.

Lender Policies

Interest rates can vary based on the lender you choose. Each lender has its policies and criteria for determining interest rates.

Factors such as the lender’s risk appetite, operational costs, and funding sources can influence the interest rates they offer. Some lenders may specialize in certain types of loans or cater to specific borrower profiles, resulting in different interest rate structures.

It is important to shop around and compare offers from multiple lenders to find the best interest rate for your mortgage. Consider working with a mortgage broker who can help you navigate the lending landscape and find the most favorable rates from a range of lenders.

Government Policies

Government programs and policies can also impact mortgage interest rates. Entities such as Fannie Mae and Freddie Mac, government-sponsored enterprises, play a significant role in the mortgage market.

Fannie Mae and Freddie Mac purchase mortgages from lenders, providing liquidity to the market and enabling more accessible mortgage financing. The rates at which Fannie Mae and Freddie Mac buy mortgages influence interest rates offered to borrowers.

In addition to these government-sponsored enterprises, there are various mortgage programs aimed at assisting first-time buyers. These programs often offer more favorable interest rates or down payment assistance to help individuals achieve homeownership.

Understanding the role of government programs and policies can help you navigate the mortgage market and identify opportunities for more favorable interest rates. Research available programs and consult with a mortgage professional to determine if you are eligible for any specific programs.

In conclusion, the determination of mortgage interest rates involves multiple factors, each with its own significance. Your credit score, loan type, economic factors, down payment, loan term, debt-to-income ratio, property type, location, lender policies, and government programs all play a role in shaping the interest rate you are offered. By understanding these factors and taking steps to improve your financial profile, you can enhance your chances of securing a mortgage with the most favorable interest rate. Remember to consult with mortgage professionals and explore all available options to make informed decisions about your homeownership journey.